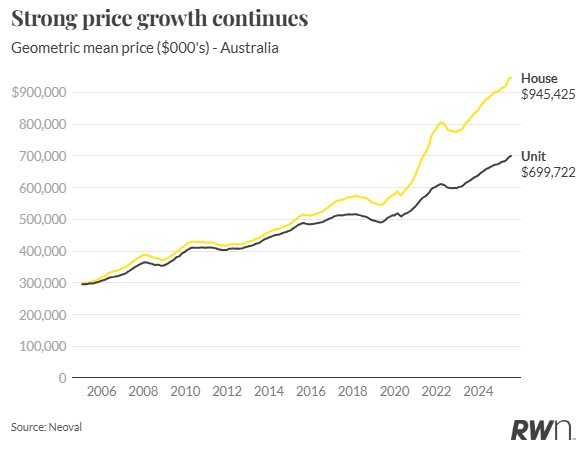

Markets show varied response to the RBA. Australia’s property market demonstrated its underlying strength in July 2025, with national house prices reaching $945,425 and unit prices achieving $699,722. The market’s resilience is evident in the long-term trajectory, with both sectors maintaining solid annual growth of 6.4 per cent for houses and 5.2 per cent for units despite the Reserve Bank’s surprise rate hold in July.

The data reveals the market’s capacity to withstand monetary policy shifts, with prices now sitting near historic highs across all markets following the dramatic recovery from pandemic lows. This trajectory reflects the fundamental supply- demand imbalance that continues to underpin price appreciation across both housing segments, positioning the market well for renewed acceleration once the anticipated August rate cuts commence.

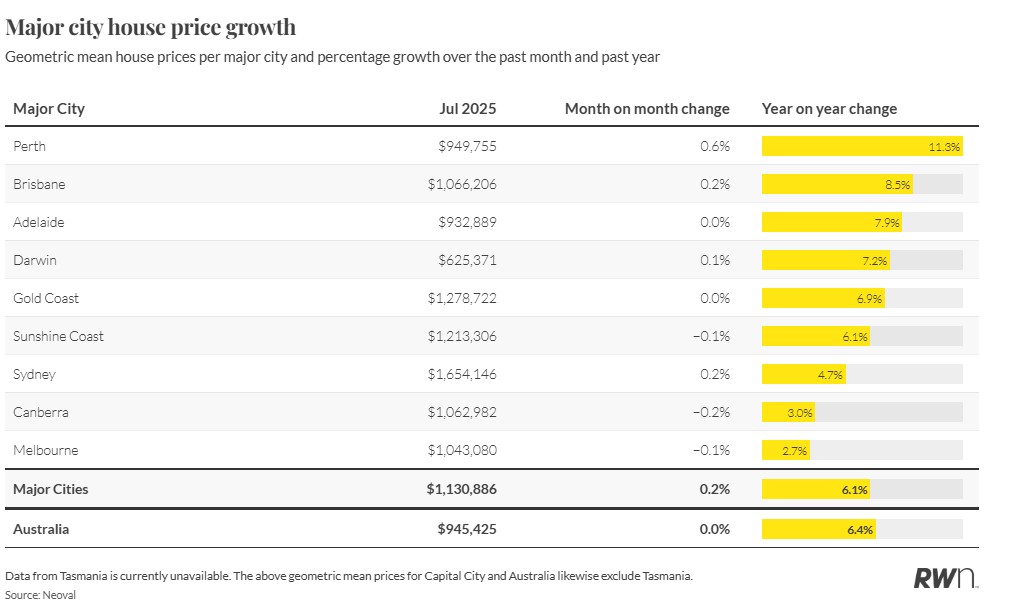

July’s metropolitan housing data reveals the immediate impact of the Reserve Bank’s rate hold decision, with markets showing varied responses to the pause in monetary easing. Perth maintained its leadership position with a mean price of $949,755, recording 0.6 per cent monthly growth and exceptional 11.3 per cent annual appreciation. Brisbane and Sydney both managed modest 0.2 per cent monthly gains, reaching $1,066,206 and $1,654,146 respectively, while their annual growth rates of 8.5 per cent and 4.7 per cent demonstrate sustained momentum.

The standout performance across smaller capitals reinforces the trend towards more affordable markets, with Adelaide, Darwin and Gold Coast all maintaining solid annual growth above six per cent. Melbourne and Canberra experienced slight monthly contractions of -0.1 per cent and -0.2 per cent respectively, reflecting their sensitivity to interest rate expectations. However, the modest nature of these declines suggests markets are positioning for the widely anticipated August rate cut cycle.

Major city unit markets showcased remarkable resilience during July’s rate hold period, with several markets posting solid gains that contrast sharply with housing sector moderation. Perth units maintained their exceptional momentum with 1.0 per cent monthly growth, reaching $626,820 and delivering outstanding 13.3 per cent annual appreciation. Brisbane and Adelaide units both recorded healthy 0.6 per cent and 0.3 per cent monthly gains respectively, demonstrating the sector’s appeal amid affordability constraints.

Sydney units provided the standout performance among the larger markets, accelerating to 0.4 per cent monthly growth and reaching $913,320, representing the only major market segment to improve during the rate hold period. This unit market strength reflects the structural shift towards higher-density living as housing affordability pressures intensify. The combined major cities unit performance of 0.3 per cent monthly growth, alongside 4.9 per cent annual appreciation, positions this sector as increasingly attractive for both investors and owner-occupiers facing price pressures in the detached housing market.

Average Milton Sale Prices August 2025

1 bed apartment $523,000 (Low $356,000 High $356,000)

2 bed apartment $740,000 (Low $840,000 High $840,000)

3 bed apartment $927,500 (No August Sales)

House $1,555,000

REA 1/9/2025